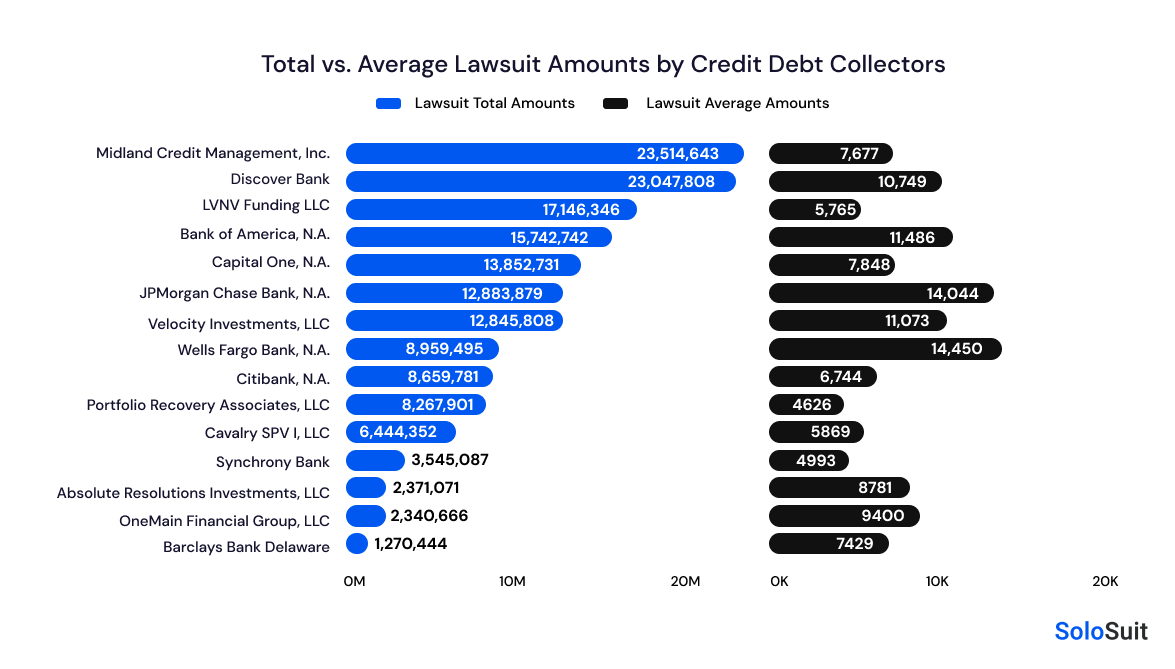

Virginia has the highest lawsuit amount, reaching an average of $49,043.

Although rare, high lawsuit amounts show how severe debt can become, especially when it grows from interest and fees, leading to significant financial challenges.

What to Do: Address large debts early by negotiating payment plans or settlements with creditors, and seek professional financial advice or legal help to avoid overwhelming debt.